")

The American Gaming Association’s latest Gaming Industry Outlook has pointed to stronger near-term conditions for the U.S. gaming industry, even as executives cite prediction markets, regulation, inflation, and geopolitical uncertainty as growing pressures on the sector.

The report, prepared with Oxford Economics, said real economic activity in the gaming industry rose 1.5% year-on-year in Q1 2026. The AGA’s Gaming Conditions Index measures gaming revenue, employment, employee wages and salaries, executive sentiment, and future event activity at casino hotels.

The U.S. economy is expected to remain resilient, supported by investment in AI and other industries. However, the report also pointed to a continued “K-shaped” economy, with lower-income households facing pressure from higher prices linked to the conflict in the Middle East, while higher-income households, benefiting from tax cuts, are expected to keep consumer spending on services positive.

The report forecast services spending growth of 2.7% in Q1 2026 and 2.4% in Q1 2027, household wealth growth of 15.8% in Q1 2026 and 3.7% in Q1 2027, and real disposable income growth of 0.7% in Q1 2026 and 2.7% in Q1 2027.

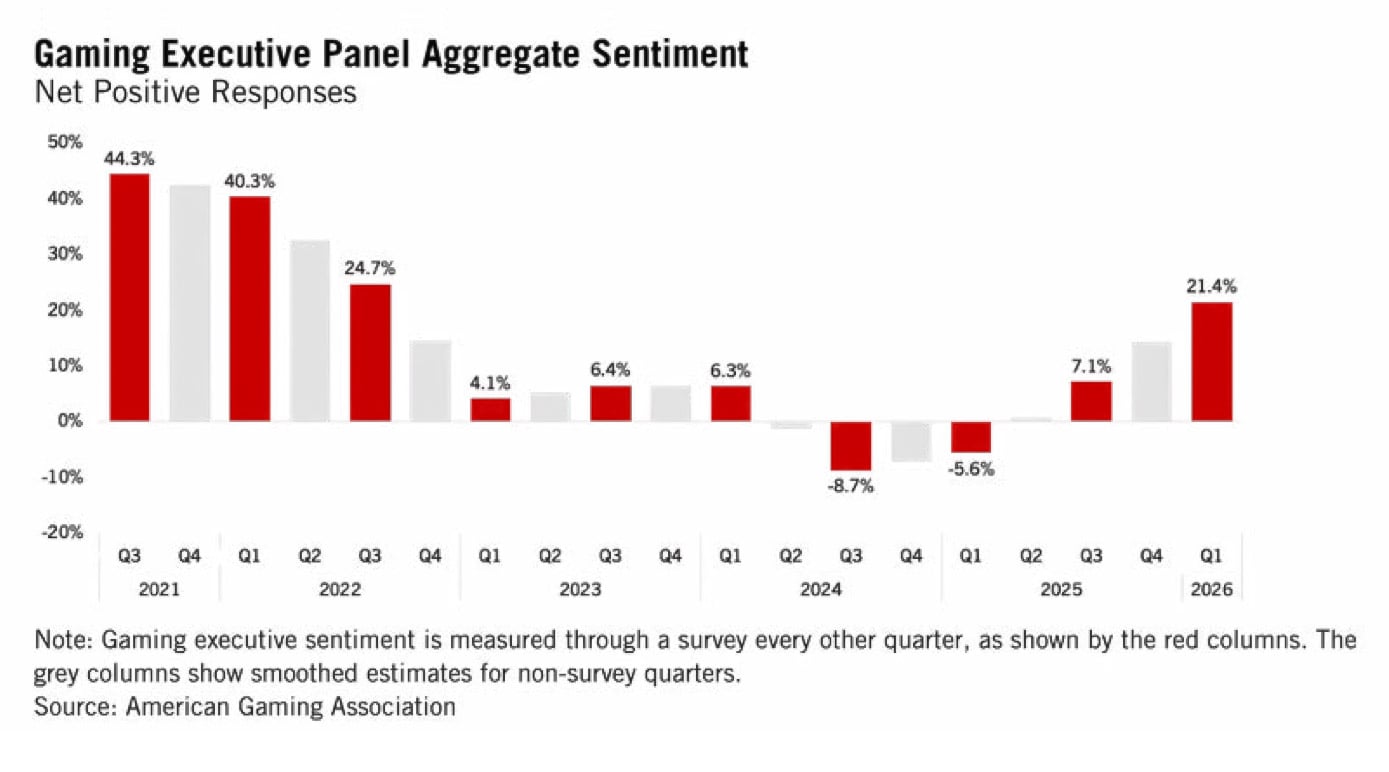

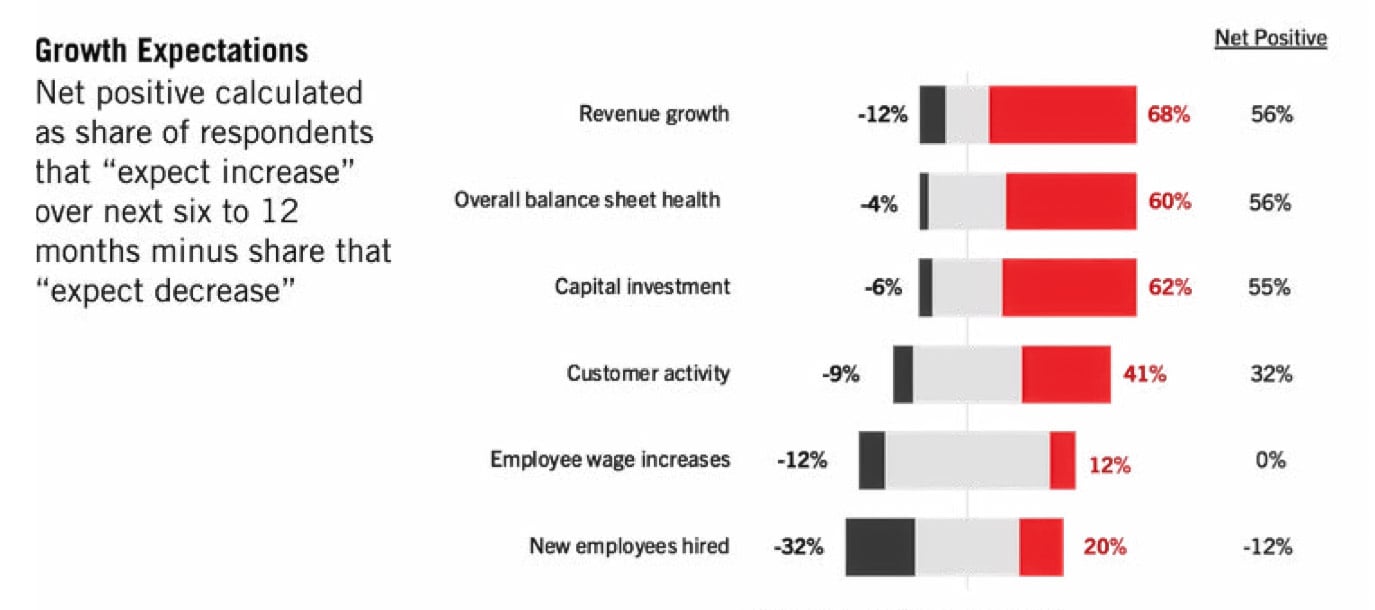

Executive sentiment also improved, reaching 21.4% net positive, the highest level since Q3 2022. More than 60% of AGA member executives expect higher capital investment, stronger revenues, and better balance sheet health over the next six to 12 months.

“The legal state and tribal-regulated gaming industry continues to demonstrate resilience and adaptability in a dynamic economic environment,” AGA CEO Bill Miller said. “Operators are focused on investing in innovation and delivering world-class entertainment, while also navigating an evolving competitive and regulatory landscape.”

The strongest expectations were recorded around revenue growth and overall balance sheet health, both at 56% net positive. Customer activity stood at 32% net positive, while 62% of executives said they expect capital investment to increase over the next six to 12 months. Half of the executives surveyed said they expect artificial intelligence to generate cost savings during the same period.

The survey also showed that executives’ assessment of the current business situation improved slightly to 12% net positive in Q1 2026, from 11% net positive in Q3 2025. However, expectations for the future business situation weakened to 8% net positive, down from 26% net positive in Q3 2025.

The report also noted that promotional activity is expected to decline for the second consecutive quarter, with executives recording a 31% net negative outlook on promotional activity.

AGA renews criticism of prediction markets

The report said prediction markets have become a major concern for regulated gaming operators. According to the survey, 81% of executives viewed prediction markets as a “very significant” threat to the regulated gaming industry.

“Illegal sports betting through sports event contracts is increasingly encroaching on legal, state, and tribal-regulated operators,” Miller said. “It’s clear the legal, regulated industry views this as a threat, and will continue to fight back and protect the integrity of our industry.”

The AGA has previously opposed sports event contracts, including through a January letter to Congress raising concerns over the Commodity Futures Trading Commission’s self-certification protocols used by prediction markets.

The association, along with the Indian Gaming Association, has argued that those protocols exploit the CFTC’s regulatory authority and undermine state law and tribal sovereignty. The AGA has also written to sports leagues discouraging partnerships with prediction markets.

The issue has also created divisions within the industry. DraftKings, FanDuel, and bet365 left the AGA partly because of the association’s position on prediction markets. DraftKings and FanDuel exited after launching their own CFTC-backed prediction market platforms.

Other operating pressures highlighted

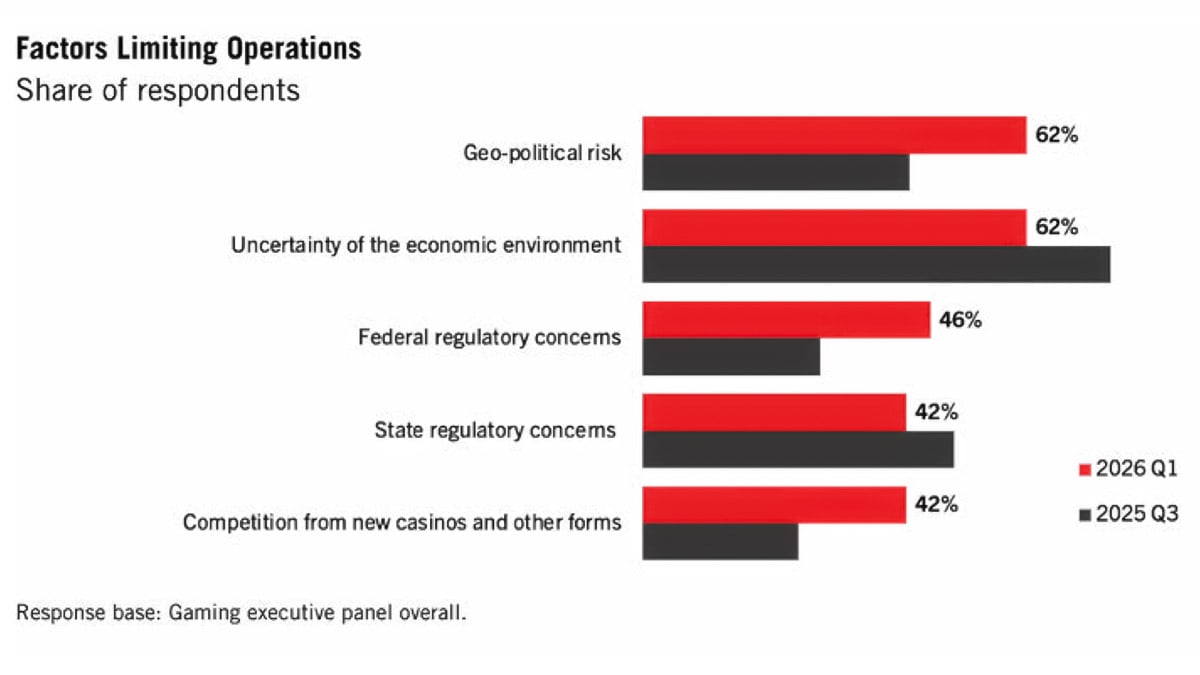

Executives also reported operating pressures. Federal regulatory concerns were cited by 46% of executives as limiting operations, up from 29% in Q3 2025. Competition from new forms of gaming was cited by 42%, compared with 25% last fall. Employee wages remained the top expense pressure, cited by 54% of respondents, while hiring expectations remained negative for the seventh consecutive survey.

Economic and political uncertainty also continued to weigh on the industry. The report cited inflation, tariffs, geopolitical conflict, supply chain pressures, the conflict in the Middle East, and higher gas prices as factors affecting margins and consumer spending.

Casino hotel event activity remained above pre-pandemic levels, with requests for proposals for business meetings and social events rising 2% from a year earlier. The report said this indicated continued demand for event bookings at casino hotels.

Among gaming equipment suppliers, sentiment also improved. Supplier expectations for capital investment reached 55% net positive, the strongest level recorded since the survey began. The report said 80% of suppliers expect increased capital investment, while 60% expect higher replacement sales and 20% expect growth in sales for new or expansion use.

The AGA noted that the outlook was based on executive sentiment, gaming activity, and economic indicators. The Q1 2026 survey included 26 gaming executives.

Original article: https://www.yogonet.com/international/news/2026/05/12/120282-aga-report-shows-stronger-gaming-outlook-despite-prediction-markets-pressure

")

{kind=link}